To estimate the workers’ compensation cost for an employee, divide their annual pay by 100, then multiply that number by your workers’ compensation insurance rate to get your estimated premium.

To estimate the average cost per employee, divide total premium by number of employees to get the average cost per employee:

(Annual Payroll / 100 * Workers Compensation Rate)

/ Number of Employees

Our online quoting tool makes it easy. Or, read on for step-by-step instructions, and other factors that play a role in your final workers’ compensation quote.

There’s no “average cost” for each employee. Every business is different, and will have a different average workers' comp cost per employee. This is because, primarily, the cost of workers’ comp coverage is based on the amount paid to each worker, and on their role or classification code.

So, for example, if you have 10 employees and pay them a combined $750,000 annually, but they're in a high-risk industry like construction, you may pay a higher average workers comp cost compared to a business that employs 20 people in clerical roles and pays $1.5 million in wages.

In addition, the average insurance cost for your company will change over time as you add and remove roles, and the wages paid go up and down, so you can expect some fluctuations. Your workers’ comp insurer will take these into account during your yearly audit to ensure that you pay the right premium.

How much does workers' comp cost per employee? The truth is, it depends — on their wages and what they do.

Workers’ compensation insurance cost is based on payroll, regardless of whether the employee is full-time, part-time, temporary or seasonal. As the formula above shows, workers’ compensation premiums are calculated in part by total payroll multiplied by the insurance rate for that class of work.

This means that the cost of workers' comp insurance per employee depends in part on what you pay them. As employees earn raises and workers come and go, your average cost of work comp per employee will fluctuate.

Want to know what you'll pay now? Here's how to find cost per employee, step by step.

To begin the process of calculating workers’ comp coverage costs, start with the gross annual earnings for each employee. This is the full amount of money they earn in a year, before any deductions. You should be able to get this information from your HR software or your payroll company.

If you can’t determine a worker’s exact earnings for the year – for example, for an hourly worker – you can estimate their projected earnings based on their hourly pay and the hours you expect them to work in a year. Your final workers’ comp cost can be adjusted based on their actual compensation at the end of the policy year.

You may also want to check your state’s requirements to see who needs to be included in your total payroll. Full-time, part-time, and seasonal workers must be covered, but in some cases, owners, partners, and family members are exempt. You also should check your state’s regulations about independent contractors, if applicable.

Need more help? Read this post: How to Calculate Payroll to Find Workers' Compensation Cost

Your classification code is one of the most important details to get right if you want an accurate workers’ compensation quote.

A classification code is a four-digit number that’s assigned to a business based on its industry. By grouping together similar businesses, data can be collected on workplace injuries and workers’ compensation claims. This data is then used by the rating agency to assess the relative risk associated with that type of work, and assign a rate based on recent losses (claims that have been filed and paid out).

With classification codes (class codes for short), insurers can assign a certain level of risk to each company based on their chances of workplace injuries.

When assigned to a business, this is called a “Governing Class Code.” Individual employees have class codes, too, but we’ll get into that a bit later.

For example, if you run a painting business, your business will be assigned the class code 5474 - General Painting Operations, since this is what describes painting businesses. You can usually find your governing class code on your current workers’ compensation policy.

Class codes don’t stop there, though. Each employee is also assigned a class code. For example, if you run a painting business, you may have a certain number of painters, who will be assigned class code 5474 - General Painting Operations.

But you may also employ a secretary or some other kind of administrative staff member. They will be assigned the class code 8810 - Clerical Office Employees.Because a painter is more likely to be injured on the job than a secretary, it’s important to make sure that each worker is classified properly so that you do not overpay (or underpay) your workers’ compensation premiums. You can take a look at this guide on how to look up class codes for more details.

To determine your classification code, consider:

WorkCompOne’s online quoting tool makes it easy: Search keywords to find your classification code — or enter the four-digit number, if you know it.

While many classification codes are standardized across the United States, workers' compensation premiums are based on the rate set by the state’s rating agency or bureau. Each class code has its own workers' compensation insurance rate.

Check with your state’s workers’ compensation regulatory body to find out which agency sets workers’ compensation rates. Many U.S. states use the National Council on Compensation Insurance (NCCI), while some use their own state rating bureau.

From there, you may be able to look up or contact the rating bureau to get the premium index rate for your classification code.

A workers’ compensation rate is represented as the cost per $100 in payroll. For example:

This will give you an estimate; not an exact quote. In most states, insurance companies are allowed to deviate from the “advised rates” published by the state’s rating agency. In some cases, the advised rate may differ greatly from the one an insurance company offers you.

For the most accurate and best price, request a quote from several insurance carriers. Or, use an independent agency, which can shop around and present you with the most competitive quote.

The state rating bureau sets the rate or baseline cost of workers’ compensation insurance by collecting and analyzing loss data—workers’ compensation claims data. This data can show patterns, such as changes in:

While rates are specific to each class code, they're often raised and lowered statewide at the same time. (For example, a statewide decrease of 3.1%.) These rate adjustments are made to reflect changes in the performance of the state’s workers’ compensation system as a whole; for example, lower healthcare costs or fewer claims as a result of improved workplace safety.

Okay, let's regroup.

So now that that you've tallied up employee wages, found your class codes and looked up your industry's workers' comp rates, you have all the pieces you need. So how do you calculate workers' compensation insurance costs per employee? Let's get into that next.

To find an estimate of cost per employee, multiply the rate by the employee payroll. You can also use the total company payroll and divide by number of employees to find the average cost per employee.

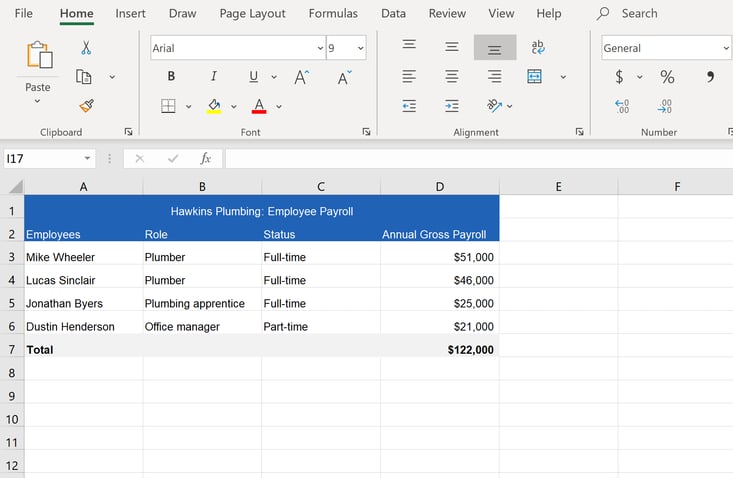

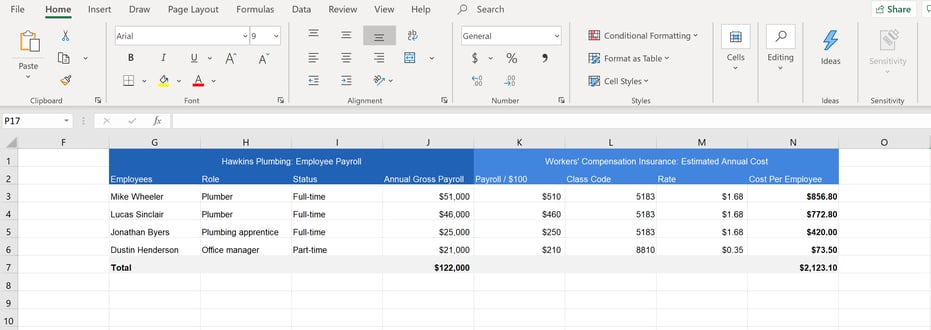

For example: This Hawkins, Indiana plumbing business has two plumbers employed, who each make approximately $50,000 per year. It also has one plumbing apprentice who makes $25,000 per year, and one part-time office manager, who handles clerical tasks and is paid $21,000 per year.

The owner enters these details into a spreadsheet to calculate the cost per employee. When added up, Hawkins Plumbing has a total payroll of $122,000 annually:

Rates are expressed per $100 in payroll, so he divides the employees' earnings by $100, then multiplies that number by the rate for each class code. The workers’ comp rate for plumbers (NCCI code: 5183) is $1.68, and for clerical or office workers (NCCI code: 8810) is $0.35.

Download a Template Spreadsheet

Also note that Dustin Henderson’s part-time employment does not impact his coverage. His full annual wages must be included, and coverage for all employees must be in effect for the entire year.

This means the formula would be the following for the three plumbers on staff:

The formula for the one clerical worker on staff would be:

We add these amounts up to find the total workers' comp policy cost:

So in total, this means that Hawkins Plumbing would be paying about $2,123 in workers’ compensation rates – which adds up to about 1.5% of their total payroll, or less than $200 per month.

It’s also important to note, in the future, these premiums could change due to a variety of factors – hiring more plumbers or administrative staff, workplace injuries, changes in total salaries paid out (raises or staff turnover), and other factors may all affect the amount that Hawkins Plumbing would pay for workers’ compensation every year.

Actual small business payroll is rarely this simple, though. So let’s look at another example, and make things a little more complicated:

Let’s say that Ken owns a motorcycle shop. Ken’s Motorcycle Shop has one full-time employee, a mechanic, and one part-time employee, a bookkeeper.

The full-time mechanic has a salary of $41,000. The part-time bookkeeper works for 10 hours per month, and makes $3,000 per year. So, how much will Ken’s Motorcycle Shop need to pay for workers’ comp coverage?

In total, Ken’s Motorcycle Shop has a payroll of $44,000. If we say that the mechanic has a rate of $1, and the bookkeeper has a rate of $0.70, we get the following results:

Due to the higher salary and higher index rate of the mechanic, the cost of their workers’ compensation coverage is much more expensive. In total, Ken’s Motorcycle Shop will pay $431 for a workers’ compensation policy. That’s an average cost per employee of $215.50, and represents less than 1% of payroll.

If we want to make things even more interesting, we can say that Ken – the owner of the business – also works full-time as a mechanic alongside his employee, and chooses to include himself in workers' compensation coverage, with an identical index rate of $1.

In most states, business owners are allowed to opt out of workers’ compensation, but if Ken chooses to cover himself with workers’ compensation, he would pay:

This means that for himself, his mechanic, and his bookkeeper, Ken would pay $1,131 for a workers’ compensation policy. That’s an average cost of $377 per employee, and represents about 1% of payroll.

Clearly, the total cost and average cost per employee are much more dependent on factors like hiring another mechanic than the bookkeeper picking up a few extra hours per week.

Workers’ compensation insurance costs are calculated based on what your business does (classification code), your total payroll and other factors the insurance carrier might use to assess your business risk (history of workers’ compensation claims, for example). And because workers’ compensation is regulated at the state level, workers’ compensation rates differ based on the state where employees work.

Your payroll and rate will give you a good estimate of workers’ compensation costs, but your final premium may look a little different. Why? There are a few different reasons:

First, there's the issue of base rate states. If operating in a base rate state, this payroll x rate formula gives you the workers’ compensation premium, before credits and debits are applied (more on that below). Base rate states require all insurers to use the workers’ compensation rates set by the state rating agency.

For those not in base rate states, insurers can deviate from the state rating bureau's published rates. This means the premium could vary based on the insurer you choose. Insurance carriers must submit their rates to the state’s regulatory body for approval, but rates may vary based on their individual history of losses.

If your business isn't in a base rate state, it's even more important to shop around for several quotes to compare, and keep in mind other factors like reputation and customer service before making a final decision.

Beyond state factors, workers’ compensation premiums are also determined by your workplace’s history of workers’ compensation claims.

A workers’ compensation rate assigns a price tag to businesses within the same industry, but workplace safety and workers’ compensation claims can vary widely from one company to the next.

For example, if you run a business with a great safety record, you may get a discount on your policy from your insurer. On the other hand, if you have a poor workplace safety record, you may end up with a higher premium from your insurer.

The insurance company may take other factors into consideration when calculating a quote, so it better reflects the characteristics of your business. Some other policy-specific factors to keep in mind include:

Based on these factors, your insurer may apply credits or debits to the premium to determine the final quote you’re offered. To save money on your workers’ compensation policy, ask an insurance agent for advice and programs or trainings that may qualify your business for savings.

While policies are nearly always active for 12 months, a workers’ compensation insurance quote might be represented as an annual premium or the monthly payment. Your preferred payment plan and any changes in your payroll throughout the year will also influence your final cost.

Some insurance carriers offer a pay-as-you-go option. Pay-as-you-go options are gaining in popularity because the employer makes payments each time they run payroll. That means the employer is only paying for what what are liable for at a given time.

As employees and wages increase or decrease, their workers' compensation premium will change.

You’ve got questions about calculating your workers’ comp premiums, and we’ve got answers. Read on for all of the details you need!

Calculating workers’ comp for part-time employees is exactly the same for part-time employees as it is for full-time employees. You’ll take their annual compensation, divide it by 100, and multiply this by the premium index rate for their role.

Of course, a part-time worker will usually have a lower average workers’ comp cost – but that’s purely because they are working fewer hours than a full-time worker. The formula for determining workers’ comp premiums remains the same.

This depends on their role, how much they're compensated, and a number of other factors, as outlined in the previous sections. However, depending on your state, you also may not be required to carry workers’ comp if you have only one employee. You can check out this guide to workers’ compensation by state for more details.

The employer must pay 100% of the cost of workers’ compensation. Businesses are not allowed to pass on any of the cost of workers’ compensation to its employees, or deduct from their wages to cover the premium. Employers in every U.S. state are required to cover 100% of worker’s compensation premiums, with no exceptions.

Yes. This means that your workers’ comp premiums are based on your employee’s wages before taxes, deductions for healthcare coverage and retirement, and other such deductions.

Your workers’ compensation premiums will vary depending on the size of your company, your industry, and other factors. However, it ends up being a very small percentage of your overall payroll.

As a simplified example, let’s say you run a company in California, which has an average premium index rate of $2.16, and you pay total gross wages of $1 million. To calculate workers’ comp premium costs, we’ll begin by dividing your payroll by 100:

Then, we’ll multiply this by the average California premium index rate of $2.16:

This means that in total, you’ll pay 2.16% of your payroll in workers’ compensation premiums.

---

Editor's note: This post was originally published in April 2019. It was updated for comprehensiveness and clarity and republished in September 2023.